Grow your bilingual chiropractic practice!

Grow your bilingual chiropractic practice: Customized images, Relevant Content, Join Community Groups, Increase website traffic. Effective and Affordable! Contact us! 651.331.8461

Grow your bilingual chiropractic practice: Customized images, Relevant Content, Join Community Groups, Increase website traffic. Effective and Affordable! Contact us! 651.331.8461

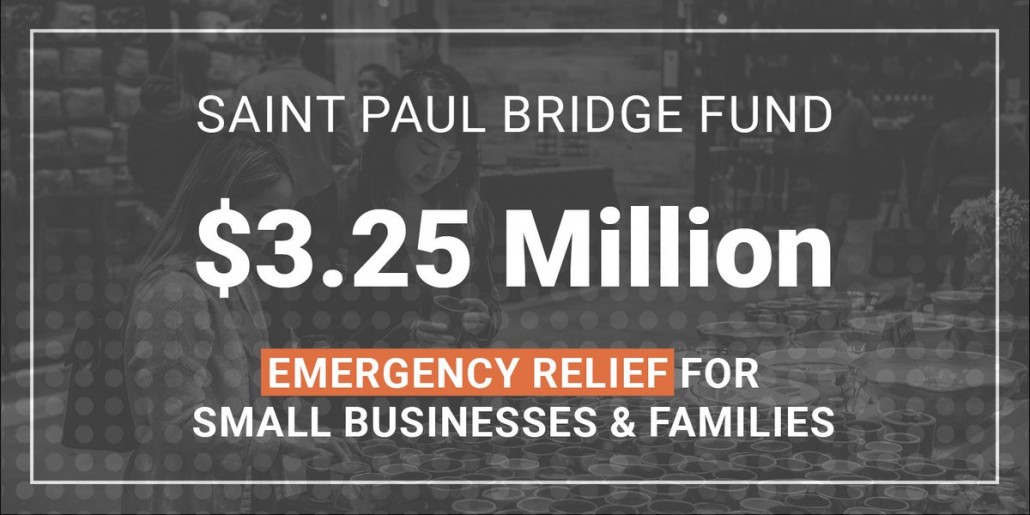

The Saint Paul Bridge Fund is an emergency relief program for families with children and small businesses impacted by the COVID-19 coronavirus pandemic. The $3.85 million fund will be distributed to qualifying Saint Paul families with children as a flat-rate $1,000 grant and to qualifying small businesses as a flat-rate $7,500 grant. It is designed to complement other state and federal emergency relief programs and ‘bridge the gap’ between now and when those dollars are available.

The $3.85 million Saint Paul Bridge Fund is supported by the Saint Paul Housing and Redevelopment Authority, and private donors including Baird, Bush Foundation, Ecolab Foundation, John S. and James L. Knight Foundation, Securian Foundation, Minnesota United FC, Minnesota Wild, the Saint Paul & Minnesota Foundation, and Xcel Energy.

Saint Paul Bridge Fund applications are open until Sunday, April 19 at 5 p.m.

If you have questions about the application or guidelines, or want help applying please call (651) 266-6565. Staff are available to help who speak English, Hmong, Spanish, Somali, Oromo and Karen.

Si tiene preguntas sobre la solicitud o necesita ayuda con la aplicacion, por favor llame al (651) 266-6565.

Yog koj muaj lus nug txog daim ntawv thiab cov cai los sis kev pab ua ntaub ntawv thov hu rau (651) 266-6565.

Haddii aad hayso su’aalo ku saabsan codsiga ama tilmaamaha, ama aad rabto caawimaad buuxinta foomka, fadlan la xariir (651) 266-6565

Qajeelfama kenname ykn unka kana ilaalchisee gaaffii yoo qabaattan bilbila kanaan gaafadhaa (651) 266-6565.

Bridge Fund for Families Application Bridge Fund for Small Businesses Application Frequently Asked Questions

For updates on the Saint Paul Bridge Fund and the City of Saint Paul’s COVID-19 response, subscribe to the COVID-19 bulletin.

Bridge Fund for Families

The Saint Paul Bridge Fund for Families is a $1 million emergency relief program for families with children impacted by COVID-19. The program provides low-income families with a flat-rate $1,000 grant for rent or mortgage payments.

Eligible families:

Saint Paul Bridge Fund for Families applications are open until Sunday, April 19 at 5 p.m.

Bridge Fund for Families Guidelines Bridge Fund for Families Application:

![]()

For Bridge Fund for Families Inquiries

Phone: (651) 266-6565

Email: residentgrant@ci.stpaul.mn.us

https://www.stpaul.gov/departments/planning-economic-development/saint-paul-bridge-fund

Bridge Fund for Small Businesses

The Saint Paul Bridge Fund for Small Businesses is a $2.25 million emergency grant program for small businesses impacted by COVID-19. The program provides small businesses with flat-rate $7,500 grant money for immediate business expenses.

Eligible small businesses are independent, for-profit, primarily retail-oriented entities registered with the Minnesota Secretary of State. In addition, they must have:

Saint Paul Bridge Fund for Small Businesses applications are open until Sunday, April 19 at 5 p.m.

![]()

Si tiene preguntas sobre la solicitud o necesita ayuda con la aplicacion, por favor llame al (651) 266-6565.

For Bridge Fund for Small Businesses Inquiries

Phone: (651) 266-6565

Email: businessgrant@ci.stpaul.mn.us

I’ve dedicated my career to understanding the Hispanic market, and I have seen it evolve, ebb and flow over time as the economy has grown. According to the Selig Center for Economic Growth, this market is on track to reach $1.7 trillion by 2020. But, if there’s one key theme I’ve seen resonate as a marketer, it’s the significant role of the Spanish language: its various uses, along with the recognition that cultural identity is bigger than knowing the language. One key understanding: Half of all second-generation Hispanics are bilingual, while only 23 percent of third generation are. There are a few themes that resonate when developing a marketing strategy for Hispanics, with language considerations woven throughout.

I’ve dedicated my career to understanding the Hispanic market, and I have seen it evolve, ebb and flow over time as the economy has grown. According to the Selig Center for Economic Growth, this market is on track to reach $1.7 trillion by 2020. But, if there’s one key theme I’ve seen resonate as a marketer, it’s the significant role of the Spanish language: its various uses, along with the recognition that cultural identity is bigger than knowing the language. One key understanding: Half of all second-generation Hispanics are bilingual, while only 23 percent of third generation are. There are a few themes that resonate when developing a marketing strategy for Hispanics, with language considerations woven throughout.

Below, I’ve offered up a few key strategies and tactics that marketers can adopt to be successful with this market, framed around their preferences for digital content, how they associate with their culture, and what types of advertising resonates with them most.

Use online video, and distribute it on mobile.

When it comes to entertainment, Hispanics love variety, and even more when it comes in the form of online video. On average, they visit nearly nine different sites, apps and services to view this content over a 30-day period. This presents a huge opportunity for marketers to implement a multi-pronged digital content strategy, where language can strategically be used across multiple touch points. Also, content that speaks to their heritage is popular with Hispanics, whether or not they’re fluent in Spanish.

A study Yahoo conducted last summer indicated that Hispanics are quickly replacing traditional television, spending a majority of their time watching online content. Moreover, they’ve become a mobile-first generation: Over the last few years, their time spent on mobile video increased by 53 percent, and is even higher for those who are Spanish-dominant, with 94 percent who watch video at least once a week. It allows them to watch whenever, wherever they are. And that’s huge for marketers.

Know your audience: Tap into Hispanics’ cultural connections.

The majority of Hispanics feel connected to their heritage. Culture is a way of life that’s felt in the way they act, what they eat, listen to, watch and how they speak with each other. There are, however, nuances between different generations. Over half of Hispanics are of millennial age or even younger, and these gaps in age have an impact on a variety of cultural factors, including language attribution, cultural identity, battling stereotypes and more.

We often hear the second-generation saying, “No soy de aqui, ni soy de alla,” which means “I’m not from here or from there” — they feel caught in between two cultures. Content needs to be tailored to their specific interests. This might mean use more ads in English, but with a stronger cultural or emotional connection — memes that play on cultural experiences or videos that poke fun can be very effective, and we see this more and more from people sharing on social media. Whomever the audience, show relatable scenarios and tug at the heartstrings.

Conversely, our study indicated the third generation feels “at home” in both cultures, having grown up primarily English-dominant, and yet still heavily connected to their heritage. They’re also more likely to feel a higher pressure for success, having learned the importance of a college education, achieving goals and living lives their parents may not have had. And when evaluating language fluency and the fact that less than a quarter of third-generation Hispanics are bilingual, marketers should assume that content that’s primarily in English, and that reinforces the attainability of the “American Dream,” will be well received with this generation.

There are also some unique instances in which the use of Spanish scales across generations. Hispanics spanning three or four generations might live under the same roof; this can mean daily interactions between grandparents, parents and their children, the latter of which might serve as interpreters for their older family members. In the digital sphere, we see social media also as a gateway for cultural connection here, as many Hispanics use different platforms to communicate with friends and family members. The opportunity here? Reinforce the heart and humor of older generations.

For advertisers, be relatable: It’s about more than translating commercials.

Here’s some music to your ears: Hispanics are very receptive to advertising; in fact, over half of millennial Hispanics actually welcome advertising targeted to them as a Hispanic. So what’s the catch? Marketers need to offer a true reflection of what it means to be Hispanic — that speaks to both Hispanic traditions and American culture. Avoid “Hispandering” — content should be highly curated and focused on cultural identity beyond just language. The use of stereotypes can be comical, but should be done properly, else they will backfire. Our third-generation study showed “Latin-style dancing” was the least important advertising element indicated by respondents.

With a larger average household size and high spending power, Hispanics are loyal to the brands they love, which creates a perfect opportunity for brand marketers. Unfortunately, too many brands expect to reach this market by pouring additional budget into their total market media buys. This is clearly not the smartest move, as this audience needs to be addressed differently. Instead, marketers should recognize barriers, and be careful and thoughtful in their strategy for this specific audience.

To recap, marketing to Hispanics requires thoughtful implementation of the following:

Use video whenever, however possible, and serve it on mobile. Whether you’re creating a short parody piece, a 30-second ad clip or a long-form feature, use video to capture attentions on every type of mobile device you can.

Know your audience! Are they Spanish-dominant? What do they read? Are they second-generation? Third? If you don’t know who you’re talking to, you won’t know how to talk to them. Because we see consumers and their interests from more points of view than any other company, we offer unique insights from 165 billion daily data events to target the right audiences.

Be real, and be credible. Hispanics are closely tied to their heritage, but that’s not all that defines them; understand where their differences lie. If possible, engage outside resources to understand these nuances; whether it’s a multicultural agency, or our insights and advertising teams at Yahoo, tap the expertise of others with a proven track record of success.

When it comes to appealing to a certain segment of any population, there’s a notable difference between knowing where people shop and what they buy. For example, knowing that 61% of U.S. Hispanic Millennials have shopped at a Hispanic supermarket once in the past year is helpful, but it’s only one layer of insight. A second layer, among myriad others, highlights that 51% of Hispanic Millennials are drawn to Hispanic grocers because they have a panadería (Hispanic bakery) or tortilla shop.

Why look at Hispanic Millennials? Because as multiculturalism and diversity gain prominence in the U.S., these young consumers will play an integral role in spending trends over the next 20-30 years. Notably, 40% of American Millennials are multicultural, and more than half of this group are Latinos. And while multicultural Millennials share the same affinity for digital technology as other the general Millennial population, more than one-fourth of all U.S. Millennials are first- or second-generation immigrants with strong ties to their global origins, which will affect their product purchases and brand loyalty.

The preferences and needs of Hispanic Millennials that Nielsen has observed are even more impactful from an opportunity perspective within certain Hispanic-rich cities like Los Angeles. Specifically, half of the Millennials in Los Angeles are Hispanic, and Nielsen expects that concentration to grow to 54% by 2020.

Nationally, 57% of U.S. Hispanics say they’re drawn to Hispanic grocers because they typically offer the products and brands that reflect their cultural tastes. What’s noteworthy is that younger Latinos, who are open to other cultures, are almost equally drawn to Hispanic grocers for the same reason (54%). The affinity for traditional Hispanic bakeries, fresh tortillas and prepared foods is strong among all Hispanics nationally.

Understanding national trends and preferences is important, but they fail to paint a complete picture of consumer behavior. Marketers know that “one size fits all” approaches won’t resonate with consumers, which is why brands and retailers need to be savvy in their efforts—and that means tailoring offerings at the local level.

For examples, groceries with a Hispanic bakery and / or tortilla shop are much more desirable among Millennial Hispanics in L.A. than they are among U.S. Hispanic Millennials. In fact, 68% of Millennial Hispanics in L.A. say they shop Hispanic groceries for this reason, well above the above the national average for Hispanic Millennials (54%). Notably, however, the presence of a wide selection of specialty Hispanic products and brands that reflect Hispanic culture are less of a draw among Millennial Hispanics in L.A. than it is for all U.S. Millennial Hispanics (46% vs. 50%, respectively).

In looking deeper at Hispanic Millennial consumption trends in L.A., we see that cultural products are strong trip drivers. In fact, they’re the No. 1 driver of trips among this group, with their baskets likely including ethnic breads like pan dulce (Hispanic sweet bread), fresh tortillas and prepared foods. Nielsen’s recent study found that Hispanic Millennials in L.A. are 26% more likely to shop specifically for Hispanic items than the city’s total Hispanic population.

Frequency is also a factor among Millennials, given this group’s tendency to pick up something and consume it that day. And in L.A., more than 50% of Hispanic Millennials spend $31 or more per trip. Notably, 64.1% of this group spends between $31 and $100 per trip. The upside here is that even though Hispanic Millennial budgets may be tighter than those of older consumers, they are attractive to retailers from a spending perspective.

Regardless of market or demographic, it’s critical for brands and marketers to know what appeals to consumers and what doesn’t. In the grocery realm, where there are millions of aisles to browse through across the country, there’s plenty of shelf space to optimize. This is particularly true when it comes to meeting the needs of Hispanics, as they do gravitate toward products and brands that are connected to their cultures—traits that many Hispanics haven’t traditionally found among some of the country’s mass-market groceries.

The insights in this article were derived from “Shopping For My Culture,” a Nielsen Hispanic Grocery Survey. The survey was in field for three weeks (from June 30, 15 to July 21, 2015) and achieved 3,307 responses, supporting the levels of analysis required for reporting. It included English-preferred, Spanish-preferred, and bilingual Hispanic households on the Nielsen Homescan Panel. The age range for Millennials is 18-34. Hispanic Grocery/Supermarket is a grocery supermarket that offers a substantial amount of products from Hispanic/Latin origin, carries Hispanic produce (fruits/vegetables), and may offer Latino bakery items, tortillas, Hispanic meat cuts or specialty products (horchata, batidos), as well as outlets also known as ethnic supermarkets.

Source: www.nielsen.com

Today, the multi-faceted Hispanic consumer is widely recognized as a cornerstone of any growth initiative for virtually all U.S. industries, and for good reason. With 57 million Hispanics in the U.S. alone, this group now represents almost 18% of the country’s population and significant spending power. In fact, Hispanic buying power reached $1.4 trillion in 2016—and we expect it to reach $1.8 trillion by 2021.

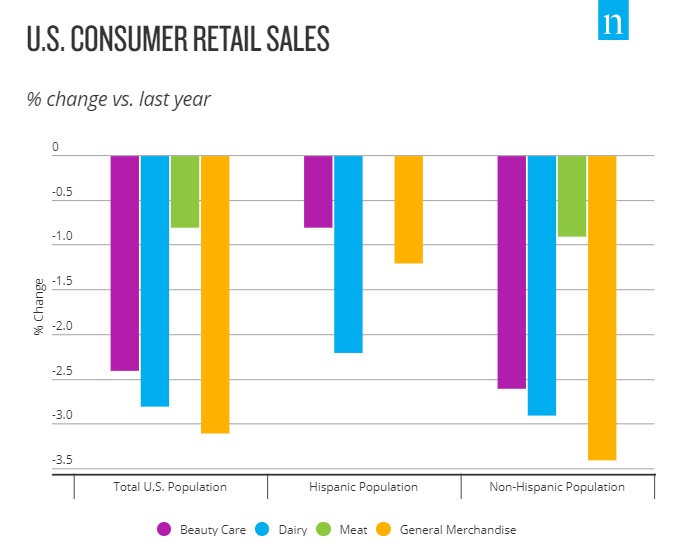

Despite concerns around the current economic and political landscape, Hispanic spending continues to rise across the total fast-moving consumer goods (FMCG) market, according to Nielsen’s Target Track retail measurement service. In year-to-date (YTD) 2017, Hispanic consumers have increased their FMCG spending by 0.6%, compared with 2016. In comparison, non-Hispanic dollars sales are 0.7% lower than last year.

However, drilling down into individual departments paints a slightly different picture in four of the 15 departments. Sales in the beauty, dairy, general merchandise and meat departments are lower YTD for both Hispanic and non-Hispanic consumers. Hispanics, however, are spending more in several key departments that non-Hispanics are pulling away from, including bakery, deli, frozen foods and household care. It’s also worth noting that sales among non-Hispanics are not growing in any department where Hispanic spend is down.

Despite shifting spending patterns, Hispanic consumers are not spending less than in previous years. At the same time, however, they’re not increasing their spend at the rate that retailers and manufacturers have become accustomed to in recent years. Across 10 of 15 key departments, YTD sales growth among Hispanic consumers are lower than they were last year. Comparatively, YTD spending among non-Hispanics is down across 12 departments.

Hispanic consumers’ overall spending has increased this year. And as Hispanic consumers drive growth, the uptick in spending is helping to partially offset the spending declines among non-Hispanics. FMCG manufacturers and retailers should note that while Hispanic consumers are continuing to spend money, they are adjusting their shopping behaviors. For example, they’re shifting to larger basket sizes per trip, suggesting the need for manufacturers and retailers to ensure that larger product formats (i.e., family size) are available to meet a growing demand.

By understanding the cultural essence that drives multicultural consumer behavior today, marketers and advertisers can forge a long-term relationships with the most dynamic and fastest growing segment of the U.S. consumer economy.

www.nielsen.com

The decline in college enrollment seems to be accelerating, though it was the steepest in the Midwest. According to experts, enrollment typically falls when the economy improves and unemployment drops. Despite a slow economic recovery and how predictable enrollment drops from an economic perspective, colleges still have to fill out classrooms to deal with increased costs or state support. Two- year colleges have seen the greatest decline; while four-year private colleges actually saw their enrollments slightly grow. What are private colleges doing differently to increase enrollment? Why aren’t most public universities and community colleges doing enough to reach out to Hispanics? After all, Hispanics are the fastest growing demographic group and due to economic and geographic reasons, Hispanics tend to choose community and technical colleges as their first choice.

Read more →

Start-Up Consulting Services

Launch Your Business the Right Way

✔ Start Your Company with Confidence

✔ Register Your Business with the State

✔ Obtain Your IRS Tax ID (EIN)

✔ Marketing Strategy & Brand Development

Who is your customer?

Success starts with the right foundation.

📍 Virtual & In-Person Services Available

📞 651-331-8461

El conferencista internacional #omarvillalobos reprograma su conferencia #atreveteaserfeliz en Minnesota hasta el 2022. Esten pendientes a futura fecha y capsulas.

Atrevete a Ser Feliz! Por Omar Villalobos Conferencista Internacional Viernes 19 Nov- 6pm-9pm Historic Concord Exchange Event Center

#socialmediamanagement fresh, relevant and bilingual content. #multivisionmarketinggroup #ClientSuccess

El ginger ayuda para la inflamación, un remedio natural que podria ayudar su dolor de espalda. #McCarronLakeChiropractic #socialmediamanagement #multivisionmarketinggroup

#socialmediamanagement fresh, relevant and bilingual content. #multivisionmarketinggroup

Affordable #socialmediamanagement: relevant, fresh, and bilingual content prepared daily for your business. #socialmediamarketing #multivisionmarketinggroup